Housing and rental stress remain the dominant economic pressures facing Australian households, with roughly two-thirds of households now exposed to elevated cost-of-living strain as inflation persists in a “higher for longer” environment.

With several economists now flagging the possibility of up to three additional 25 basis-point interest rate increases in 2026, the distributional impact of further monetary tightening warrants closer examination.

Each incremental increase is estimated to add approximately $120–$160 to median monthly mortgage repayments, compounding stress in electorates already characterised by high mortgage exposure and constrained housing supply.

Against this backdrop, this analysis examines how rising household financial vulnerability under renewed monetary tightening may translate into electoral opportunity for One Nation (ONP), particularly given its already elevated primary vote across a significant number of electorates at the 2025 federal election.

ONP Baseline: Top 30 Unsuccessful Electorates by Primary Vote (2025)

The table below presents ONP’s top 30 primary vote results in electorates it did not win at the 2025 House election, alongside the successful seat holder.

Top 30 electorates by ONP primary vote (2025 House) + seat holder

| Rank | Division | State | ONP votes | ONP primary % | Seat holder (successful party) |

| 1 | Wright | QLD | 18,998 | 15.26% | Liberal National Party of Queensland |

| 2 | Capricornia | QLD | 15,355 | 15.02% | Liberal National Party of Queensland |

| 3 | Hunter | NSW | 18,011 | 14.83% | Australian Labor Party |

| 4 | Gippsland | VIC | 15,118 | 13.91% | The Nationals |

| 5 | Flynn | QLD | 13,874 | 13.27% | Liberal National Party of Queensland |

| 6 | Hinkler | QLD | 14,498 | 12.64% | Liberal National Party of Queensland |

| 7 | Brand | WA | 11,960 | 12.32% | Australian Labor Party |

| 8 | Parkes | NSW | 14,320 | 12.27% | The Nationals |

| 9 | Maranoa | QLD | 12,018 | 11.63% | Liberal National Party of Queensland |

| 10 | Wide Bay | QLD | 12,646 | 11.50% | Liberal National Party of Queensland |

| 11 | Canning | WA | 11,488 | 11.04% | Liberal |

| 12 | Nicholls | VIC | 12,095 | 10.90% | The Nationals |

| 13 | O’Connor | WA | 11,053 | 10.45% | Liberal |

| 14 | Mallee | VIC | 11,414 | 10.26% | The Nationals |

| 15 | Dawson | QLD | 10,258 | 9.93% | Liberal National Party of Queensland |

| 16 | Corio | VIC | 10,953 | 9.62% | Australian Labor Party |

| 17 | Forde | QLD | 11,049 | 9.61% | Australian Labor Party |

| 18 | Longman | QLD | 12,062 | 9.50% | Liberal National Party of Queensland |

| 19 | New England | NSW | 11,387 | 9.48% | The Nationals |

| 20 | Burt | WA | 9,789 | 9.47% | Australian Labor Party |

| 21 | Durack | WA | 8,868 | 9.44% | Liberal |

| 22 | Hawke | VIC | 10,035 | 9.27% | Australian Labor Party |

| 23 | Grey | SA | 10,652 | 9.26% | Liberal |

| 24 | Groom | QLD | 9,860 | 9.09% | Liberal National Party of Queensland |

| 25 | Blair | QLD | 11,344 | 9.06% | Australian Labor Party |

| 26 | Pearce | WA | 9,089 | 8.98% | Australian Labor Party |

| 27 | Spence | SA | 10,654 | 8.77% | Australian Labor Party |

| 28 | Riverina | NSW | 10,427 | 8.74% | The Nationals |

| 29 | Lingiari | NT | 4,132 | 8.65% | Australian Labor Party |

| 30 | Shortland | NSW | 9,813 | 8.55% | Australian Labor Party |

Why the 10% Primary Threshold Matters

A primary vote above 10% is commonly understood as a threshold at which vote reallocation and preference influence become electorally material, particularly under conditions of heightened economic stress.

At the 2025 election, ONP recorded 14 electorates above the 10% primary threshold, prior to any additional tightening or renewed inflationary pressure. Notably, 12 of these seats were held by the Liberal or National parties, with only two held by Labor — indicating that ONP’s baseline strength is disproportionately concentrated in Coalition-held territory.

This is occurring against a backdrop of persistently high CPI and population-driven demand pressures, where higher immigration intake continues to place upward pressure on housing, transport infrastructure, and service provision — dynamics that are felt unevenly across electorates.

Coalition Vote Retention Under Pressure

Recent Roy Morgan polling indicates declining voter confidence in both the Liberals and Nationals. While individual polling movements should not be over-interpreted, the consistency of direction across multiple weeks suggests a non-random and potentially sustained shift in voter sentiment.

Over the past two months — a period that included the Bondi terror attack — Coalition support has deteriorated materially:

- Liberals: 23% → 18%

- Nationals: 3.5% → 2.5%

- Labor: 32% → 30.5%

By contrast, ONP’s primary vote increased from 15.5% to 25% over the same period.

| Primary Vote | Dec 2025* | Jan 2026* | Late Jan 2026* | Early Feb 2026* | Change |

| 4 Wks* | 4 Wks* | 1 Wk* | 1 Wk* | ||

| % | % | % | % | % | |

| ALP | 32 | 30 | 30.5 | 30.5 | – |

| One Nation | 15.5 | 21.5 | 22.5 | 25 | +2.5 |

| Liberal | 23 | 21 | 20 | 18 | -2 |

| National | 3.5 | 3 | 2.5 | 2.5 | – |

| Greens | 13.5 | 12.5 | 13 | 12.5 | -0.5 |

| Independents/Others | 12.5 | 12 | 11.5 | 11.5 | – |

| TOTAL | 100 | 100 | 100 | 100 |

Source: Roy Morgan

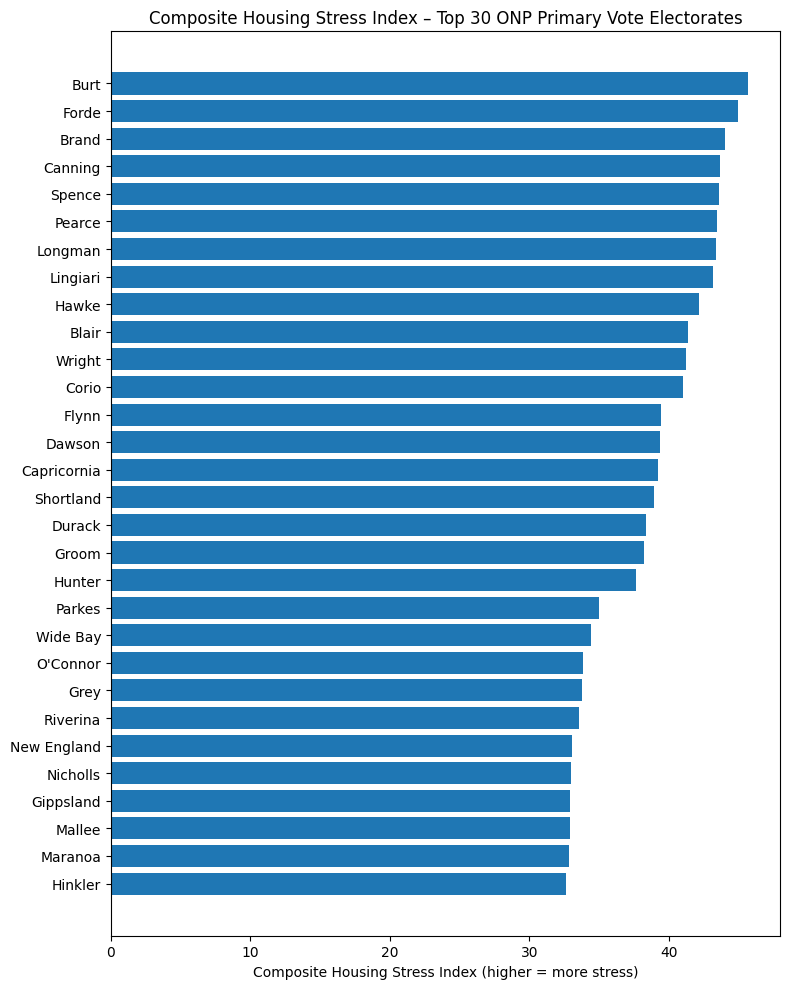

Mortgage Stress Sensitivity in High-ONP Electorates

Using 2021 Census mortgage repayment data, uprated to reflect current interest rate settings, mortgage stress was modelled across ONP’s top 30 primary vote electorates under a three-hike (+0.75%) scenario.

Five electorates emerge as high mortgage stress (40%>)and most sensitive to further tightening:

- Burt

- Brand

- Canning

- Forde

- Spence

Three of these seats — Burt, Brand, and Spence — are Labor-held, with ONP primary votes ranging from 9.47% to 12.7% at the 2025 election.

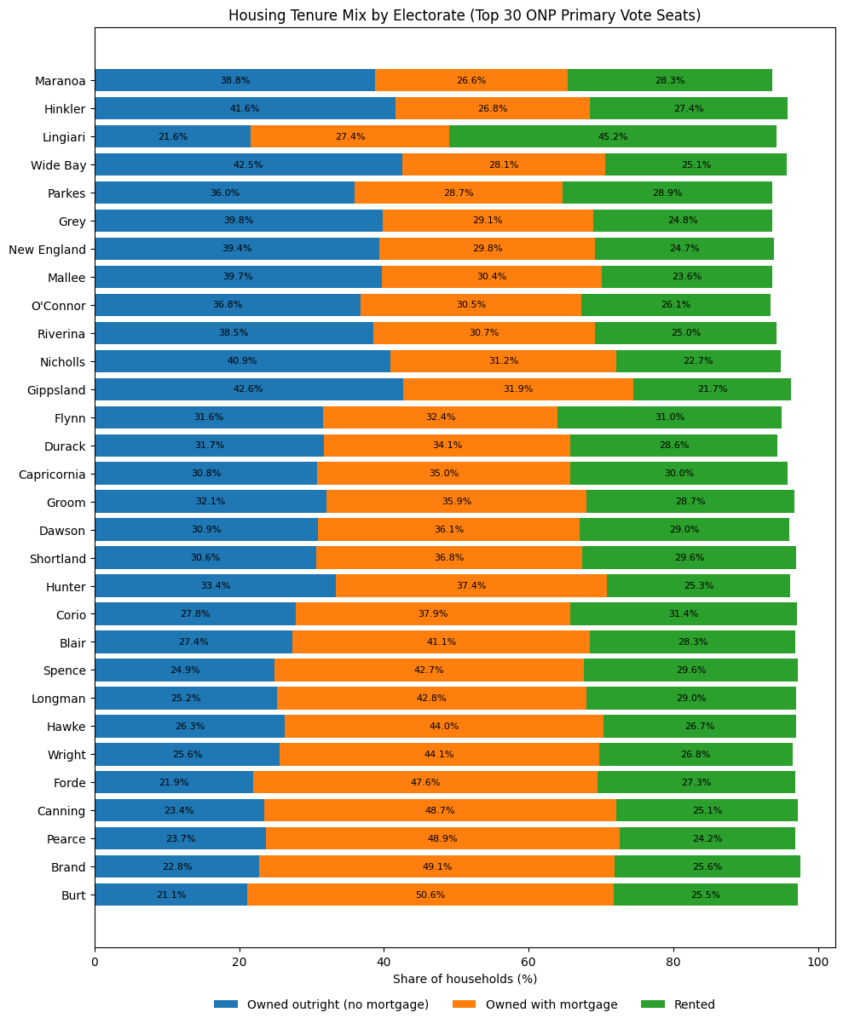

Demographic Exposure: Younger, Mortgaged, Politically Volatile

All three Labor-held electorates (Spence, Brand, and Burt) have a median age of approximately 35, closely aligned with the current median age of first-home buyers. Estimated 2025 median mortgage sizes in these seats range from ~$572,000 in Spence to ~$730,000 in Brand and Burt, placing households in these electorates among the most interest-rate-sensitive in the country.

This demographic profile contrasts sharply with ONP’s strongest regional seats — such as Hinkler, Wide Bay, and Gippsland — where home ownership without a mortgage is more prevalent, median ages range from 46–49, and ONP’s primary vote sits between 11.5% and 13.9%.

Two ONP Voter Coalitions, Not One

This divergence highlights an important structural shift:

ONP is no longer appealing to a single demographic bloc.

- Older regional electorates: higher outright ownership, policy salience around health services, agriculture, regional infrastructure, and cost containment.

- Younger outer-metro electorates: high mortgage penetration, rising debt loads, and acute sensitivity to monetary tightening.

The largest concentration of owner-occupiers with mortgages across ONP’s high-primary electorates sits between 41.1% and 50.6%, creating a clear channel through which interest rate policy directly intersects with voting behaviour.

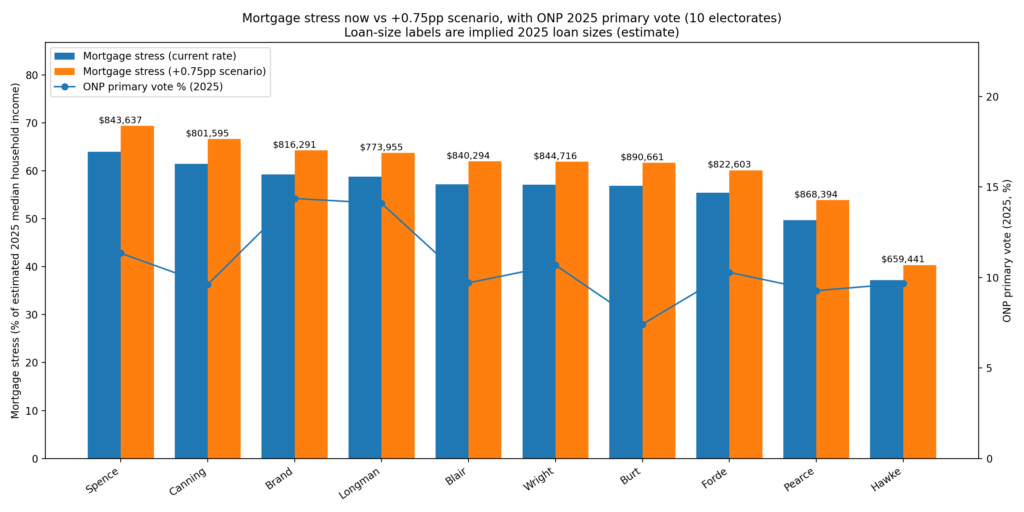

Finally, the analysis presents a composite view of One Nation’s top ten primary-vote electorates, combining current mortgage stress, estimated average mortgage size, and the projected increase in mortgage stress under a +0.75 percentage-point interest rate scenario, with ONP primary vote share overlaid.

The resulting pattern indicates that ONP’s strongest recent gains increasingly coincide with electorates characterised by high mortgage exposure and younger age profiles. This alignment suggests a potential expansion of ONP’s electoral base beyond its traditional older, regional constituency, toward mortgage-burdened Millennial and Gen Z voters.

In this context, policy messaging centred on household balance-sheet security, fiscal restraint, and opposition to cost-inflating settings may resonate with younger cohorts whose voting behaviour is increasingly shaped by housing affordability and debt serviceability rather than cultural alignment alone.

As an end note, when interest rates become the loudest voice in the room, classic two-party political ideology takes a back seat to survival — and protest voting stops being a tantrum and starts looking like a rational response. One Nation’s advantage isn’t persuasion; it’s being the only party not pretending Australia isn’t edging toward a serious economic collision course, while actively inviting economic discourse from stakeholders and the public, rather than relying on PR to brigade against the realities of the current economic environment.