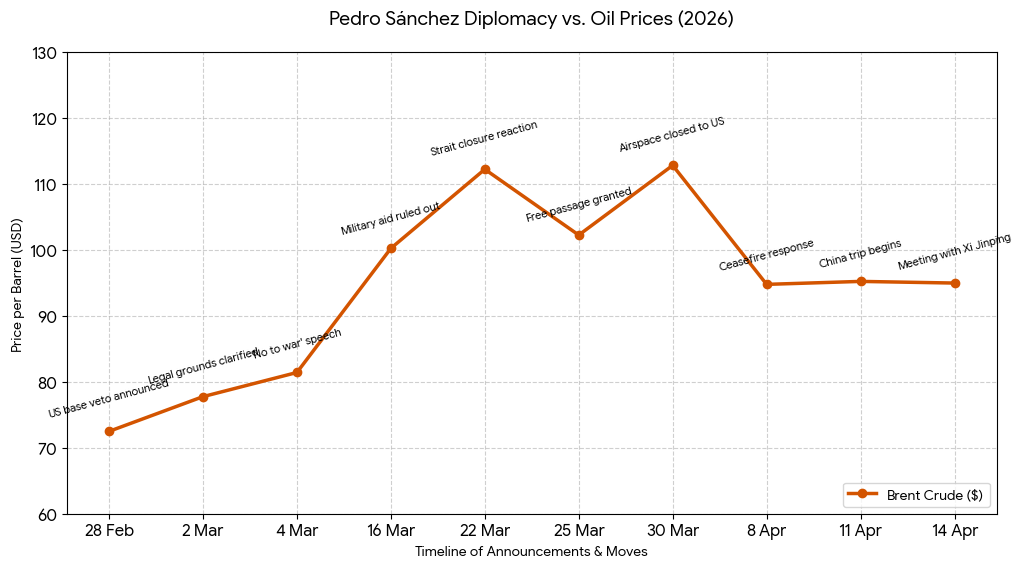

On Saturday, 28 February 2026, Spain’s Prime Minister Pedro Sánchez announced that US forces were prohibited from using the Rota (Cádiz) and Morón (Seville) bases.

Foreign Minister José Manuel Albares reinforced this announcement on Monday, 2 March 2026.

The following weekend, 15 US aircraft departed Spanish bases.

On Wednesday, 4 March, Sánchez delivered a televised address reiterating his “No to war” stance after US President Donald Trump threatened to cut off trade with Spain in retaliation for the base veto.

This occurred during the fifth day of the closure of the Strait of Hormuz.

On 16 March, Sánchez rejected military aid, officially ruling out participation in any mission to secure the Strait of Hormuz, calling the US–Israeli campaign “illegal.”

On 25 March, the Majorca Daily Bulletin reported that Iran granted Spanish ships “free passage” through the Strait, designating Spain a “non-hostile” country.

This was later echoed by the Iranian embassy in Spain as a gesture of goodwill toward Sánchez’s anti-war stance.

This framing positioned Spain among other “non-hostile” nations such as India, China, Turkey, and Malaysia, while core aligned nations such as China, Russia, India, Pakistan, and Iraq remain consistently welcomed.

However, it is worth noting that Spain’s own Foreign Ministry stated it had no prior knowledge of the announcement when contacted by media. This suggests it may have been a unilateral Iranian statement rather than a confirmed bilateral agreement.

As of now, Spain has yet to utilise the Strait for ship passage under this arrangement.

Now I’ve formed a graph to see how Pedro’s diplomatic announcements & timeline have impacted the oil market.

From 11–15 April, Sánchez is visiting Beijing for his fourth trip in three years. During a meeting with Xi Jinping, Sánchez stated that China is the “only global player” capable of resolving the Iran – Hormuz crisis. Reviewing China’s official statement from this meeting, there is a clear positioning of China as a defender of international law through multilateral trade frameworks, with an underlying intent to compete with the US petrodollar system.

However, recurring language such as “One China principle” and “territorial integrity” may be interpreted as strategically assertive, particularly by markets in Japan, South Korea, and Taiwan.

Overall, the statement reads more as a broad geopolitical posture of strength for the Chinese rather than a focused framework for developing specific economic ties with Spain.

That said, the multilateral relationship could still support Spain’s economic position. Trade between Spain and China currently sits at approximately $50 billion (2025).

However, as seen in Australia, overreliance on China can create structural vulnerabilities — particularly around supply chains, green energy dependency, and exposure to economic coercion.

Prior to this visit, several outlets reported unconfirmed speculation that Spain may consider utilising the “petroyuan” for trade and passage through the Strait.

At present, this appears to be speculative and may function as a market test to gauge both domestic and international reaction. It has not yet been confirmed.

Currently, Sánchez’s national polling sits at approximately:

- 25% preferred Prime Minister

- PSOE: 27–32%

- Alberto Núñez Feijóo’s People’s Party: 30–32%

If an election were held today, the PP would likely form government.

In relation to China’s positioning against the US petrodollar, it is also relevant to consider its statement released the same day following a meeting with Khaled bin Mohamed bin Zayed Al Nahyan.

In contrast, China’s tone toward’s Abu Dhabi is notably more direct and constructive, outlining clearer intentions around energy stability, security architecture, and willingness for regional cooperation.

Xi presented a four-point proposal centred on peace and stability in the Middle East, with emphasis on sovereignty and reduced reliance on external military powers.

The Crown Prince’s response highlighted mutual trust and a willingness to deepen coordination with China, particularly around maintaining shipping security.

Comparing both statements, there is a noticeable difference in strategic weight.

China’s engagement with the Middle East appears more substantial and willing, while its positioning with Spain remains more generalised.

This suggests a current communications prioritisation of resource-rich and strategically critical regions over politically uncertain Western economies.

From a broader perspective, weaker polling positions in countries such as Spain, the UK, Canada, and Australia may present economic vulnerabilities.

There is an argument that these conditions create opportunities for external powers like China to establish deeper economic influence, particularly where leadership continuity is uncertain.

As seen in Australia over the past two decades, this can lead to increased dependency and reduced economic flexibility over time.

The past two months of Pedro Sánchez’s diplomatic activity provide a useful case study in how markets react when a major EU economy starts drifting toward a more neutral — and at times anti-US — position.

Right now, it’s all signalling.

Whether it becomes strategy or just noise will come down to execution, and whether Spain can actually convert this positioning into something economically durable before the political cycle catches up, it is most interesting none the less.